Published 17:15 IST, April 29th 2024

Old vs new tax regime: Know what's better for salaried employees

Here's a quick comparison of both tax regimes to help you make an informed decision.

Advertisement

Old vs New Tax Regime: Are you scratching your head, confused between the choice of sticking with the tried-and-tested old tax regime or succumbing to the enticing allure of the new regime? Here's a quick comparison of both tax regimes to help you make an informed decision.

Budget 2023 introduced key changes to incentivise the adoption of the new regime. Notably, the higher tax rebate limit, now applicable for incomes up to Rs 7 lakh compared to Rs 5 lakh under the old regime, provides relief for taxpayers. Moreover, the revised tax slabs and extended deductions, including the standard deduction for salary income, contribute to making the new regime more appealing.

Advertisement

Conversely, the old tax regime retains its allure with over 70 exemptions and deductions, including the popular Section 80C, allowing for substantial reductions in taxable income. This familiarity and the potential for significant tax savings make the old regime a compelling choice for many taxpayers.

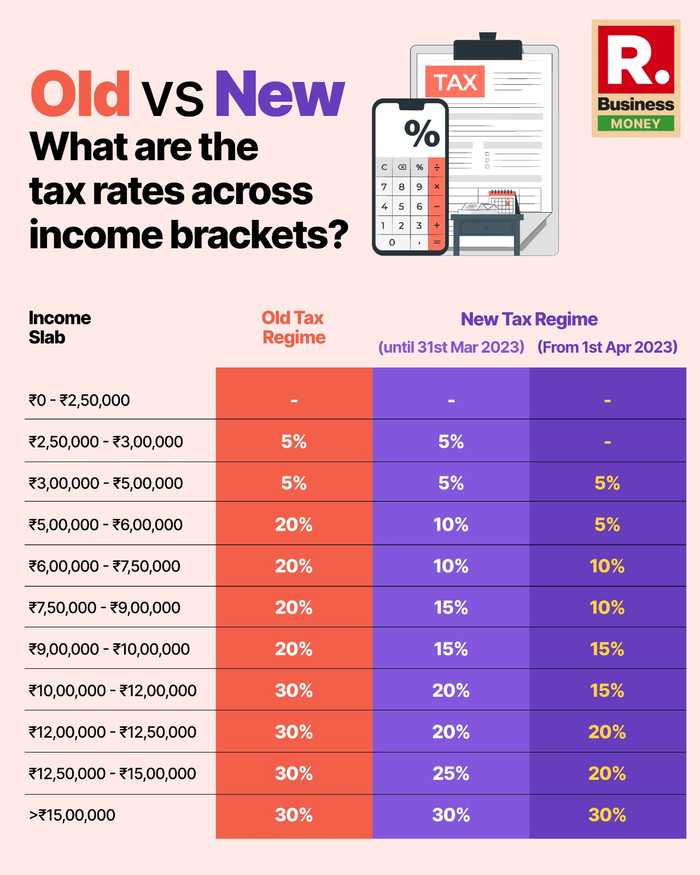

Old vs New: What are the tax rates across income brackets?

The tax rates under three different regimes, namely the old tax regime, the new tax regime until March 31, 2023, and the new tax regime from April 1, 2023, are compared across various income slabs. Under the old tax regime, there are no tax implications for income up to Rs 2,50,000. However, in the new tax regime until March 31, 2023, and the one from April 1, 2023, the tax rate remains at 5 per cent for the income slab of Rs 2,50,000 to Rs 3,00,000.

Advertisement

For incomes between Rs 3,00,000 and Rs 5,00,000, the tax rate is 5 per cent under all three regimes. Notably, the new tax regime from April 1, 2023, introduces changes in tax rates for higher income slabs. For instance, under the old tax regime, the tax rate for incomes between Rs 5,00,000 and Rs 6,00,000 is 20 per cent, which reduces to 10 per cent in the new regime until March 31, 2023, and further decreases to 5 per cent under the new regime from April 1, 2023. Similarly, tax rates for other income slabs also vary across the three regimes, reflecting adjustments aimed at altering the tax burden for different income groups.

Under the new tax regime, the standard deduction of Rs 50,000, previously exclusive to the old regime, has been extended, making Rs 7.5 lakh the tax-free income threshold. Additionally, individuals receiving family pensions can claim a deduction of either Rs 15,000 or 1/3rd of the pension, whichever is lower.

Advertisement

Notably, high net worth individuals benefit from a reduced surcharge rate on income exceeding Rs 5 crore, dropping from 37 per cent to 25 per cent. This reduction results in a decrease in the effective tax rate from 42.74 per cent to 39 per cent. Furthermore, non-government employees can now enjoy a higher leave encashment exemption, soaring from Rs 3 lakh to Rs 25 lakh, marking an eight-fold increase.

Fiscal default switch

Effective from the fiscal year 2023-24, the new income tax regime is set as the default option, requiring individuals who opt for the old regime to submit their income tax returns alongside Form 10IEA before the due date. However, taxpayers retain the flexibility to switch between the two regimes annually to assess potential tax benefits.

Advertisement

Traditional tax perks

The old tax regime, characterised by over 70 exemptions and deductions including HRA and LTA, offers avenues for reducing taxable income and lowering tax liabilities. Notably, Section 80C remains a prominent deduction, allowing for a maximum reduction of taxable income by Rs 1.5 lakh.

Individuals are presented with a choice between the old and new tax regimes, with the decision hinging on the tax-saving deductions and exemptions available under each.

Advertisement

09:23 IST, April 29th 2024