Published 22:45 IST, February 22nd 2024

Anglo American CEO has seen the miner’s share price more than halve since taking over in 2022,

Advertisement

True gem. Duncan Wanblad ought to look to his predecessor for ideas. The CEO of $30 billion Anglo American has seen the miner’s share price more than halve since taking over in April 2022, with another 21% off since December after the miner disappointed on production volumes. Former Anglo boss Mark Cutifani’s latest job at Brazilian miner Vale may offer some inspiration for how to stop the rot.

In 2016, Cutifani resolved to strip Anglo down to copper, diamonds and platinum to reduce its debt pile, only for the plan to be shelved when prices of what he was proposing to exit surged. In 2024, Wanblad has two problems – a slump in diamond prices caused partly by lower demand from Chinese consumers, which prompted 2023 group EBITDA to slump by 31% and prompted $1.6 billion of impairments – and a yawning conglomerate discount.

Advertisement

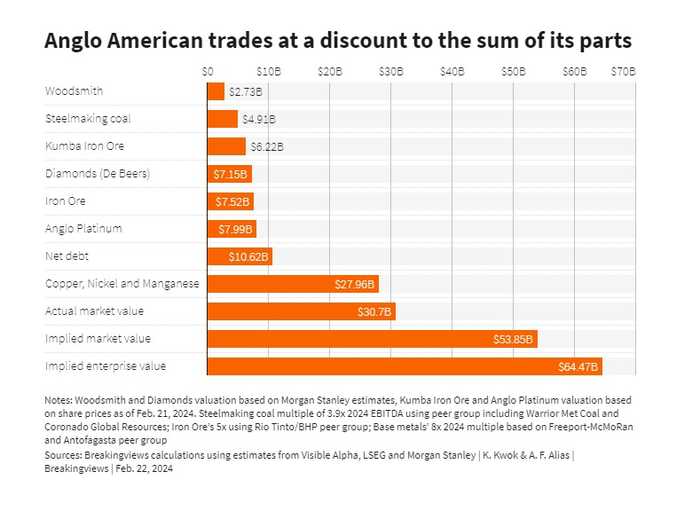

Of the $10 billion of EBITDA Anglo is expected to make in 2024, on Visible Alpha estimates, $3.5 billion could come from base metals – copper, nickel and manganese – with another $1.5 billion from iron ore and $1.3 billion from steelmaking coal. Placing them on peer group multiples implies valuations of $28 billion, $8 billion and $5 billion respectively, according to Breakingviews calculations. Add in another $8 billion and $6 billion to reflect the observable values of the miner’s listed Anglo American Platinum and Kumba Iron Ore units in South Africa, and that implies an enterprise value of $55 billion. That compares to Anglo’s current value at $41 billion including net debt, and doesn’t even include De Beers, which Morgan Stanley reckons could be worth $7.1 billion, or its UK fertiliser project Woodsmith.

One obvious step might be to spin off or sell Anglo’s 85% stake in low-margin De Beers. But it’s not a great time to do so, and it’s politically tricky: the remaining 15% is held by the Botswanan government. Hiving off the platinum and Kumba parts might also raise politicians’ hackles if it made London-listed Anglo less South African.

Advertisement

That’s where Cutifani’s lead might help. The ex-Anglo boss chairs Vale Base Metals, a new Toronto-based entity with a separate board that’s likely to list in the coming years. As with Canada’s Teck Resources, Vale has been trying to drive value by splitting the base metals business, which is set to motor due to demand for its products via the green transition, from the rest of its group.

Such a move wouldn’t be a panacea. Copper prices are currently subdued, and mines need capital investments to operate. But here Vale might again provide handy context. Last July the Brazilian group raised $3.4 billion by selling a 13% stake in Vale Base Metals to Saudi Arabia and other transition-focused investors. If Wanblad could find a similar pot of cash and set up a new base metals entity sporting a $28 billion valuation, his sorely needed revamp might gain some impetus.

Advertisement

22:45 IST, February 22nd 2024