Published 17:01 IST, October 29th 2023

A close look into the latest investments by oil giants Exxon Mobil and Chevron.

Advertisement

Pocket change. Exxon Mobil and Chevron are sending prodigious amounts of cash to investors, but third-quarter results show how quickly priorities can start to compete. The two companies reported somewhat similar results on Friday, with the $420 billion Exxon earning $9.1 billion, and the $279 billion Chevron making $6.5 billion. Both companies’ profit shrunk compared to the same period last year, thanks to lower commodity prices. With more than $110 billion in acquisitions between the two of them, investors might wonder where they will slot in.

Exxon returned over $8 billion to investors and Chevron $6 billion, and right now that’s not at the expense of their balance sheets. Exxon’s cash pile is closing in on its long-term debt. Chevron’s total debt is less than a tenth of its overall value.

Advertisement

But investment is rising. Exxon said that its full year capital and exploration expense will probably be near the top of its guidance of up to $25 billion. Chevron has spent $11.5 billion so far this year, over 40% more than last.

The giants are also flexing their deal muscles, with Chevron announcing a deal to buy Hess for $53 billion in stock, and Exxon acquiring Pioneer Natural Resources for $60 billion. Over the past decade both stocks have sharply underperformed the S&P 500 Index as they’ve grown their positions dramatically. The best time for discipline is when cash is flowing. (By Robert Cyran)

Advertisement

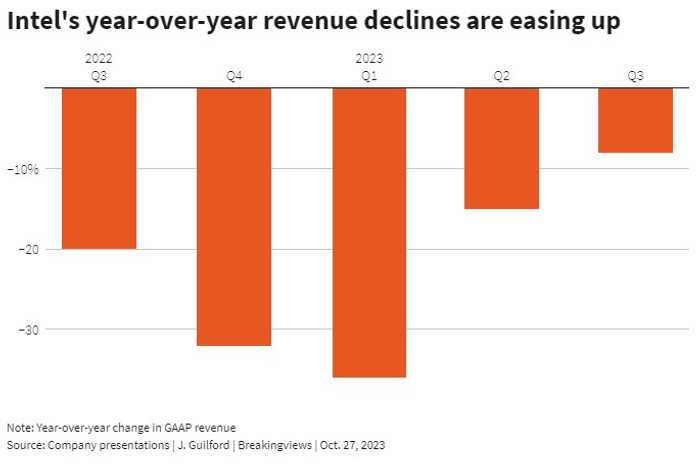

Turnarounds. Intel boss Pat Gelsinger has gotten a rare break. The $150 billion chip giant has weathered a post-Covid maelstrom as an initial work-from-home-driven boost to PC sales slammed into reverse, denting sales and the company’s chunky gross profit margin. Growth isn’t back, but results released on Thursday show the decline is slowing and a new division has promise. At least one pandemic bullwhip might be close to having run its course.

Intel needs cash, and lots of it, for investments to regain a technological lead lost to arch-rival Taiwan Semiconductor Manufacturing. The PC market’s collapse has complicated that task, with slumping demand leading to under-utilized factories and consequently lower profit. But things might be stabilizing: gross margin jumped to 43% from 36% last quarter, while revenue declines are steadily tailing off.

Advertisement

Better yet, Intel’s foundry business - Gelsinger’s push to start making chips designed by others - is narrowing its losses while growing revenue and scaling up. This helped the company’s stock gain 10% on Friday. Though many customers are signing up on the condition that Intel’s manufacturing tech reaches certain milestones, that unit is its future. With no new surprise delays and the company’s numbers trending in the right direction for a change, the path to getting there looks a little more achievable than it did a day ago. (By Jonathan Guilford)

Long recovery. Sanofi investors dislike CEO Paul Hudson’s prescription to reinvigorate the pharmaceutical group’s weak valuation. Shares in the $130 billion French drug giant dropped 15% on Friday after it said it would ramp up research and development spending to build a better pipeline of future drugs. That will cause 2024 earnings to fall at a low single-digit rate compared to 2023 levels before a “strong rebound” in 2025, the company said. Part of the strategy also involves spinning off Sanofi’s consumer health unit as soon as the fourth quarter of 2024.

Advertisement

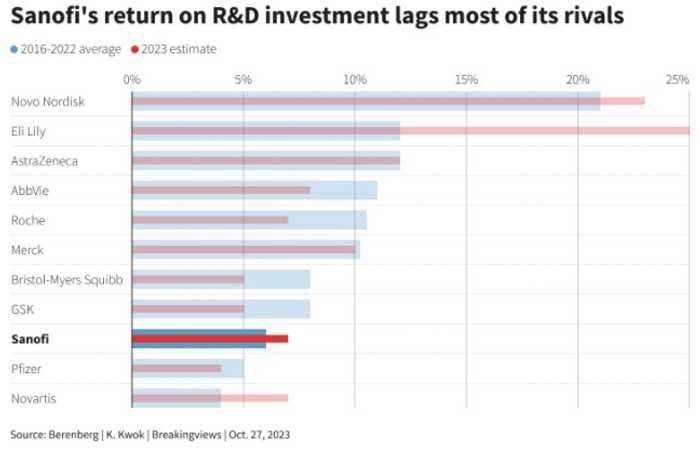

Focusing on finding new blockbuster medicines makes sense. Overall, the industry is facing the expiry of patents stretching to the end of the decade, which exposes $200 billion of top-selling branded drugs to competition and will squeeze revenues, according to Ernst & Young. But investors’ concern is also understandable given that Sanofi has extracted below-par returns from its R&D investments: between 2016 and 2022 Sanofi returned roughly 6% a year on average, below the 10% reaped by the sector as a whole, according to Berenberg analysts’ estimates.

That explains why the stock’s price-to-earnings multiple is also trading below most of its rivals. Spinning off Sanofi’s consumer healthcare business would help. Analysts polled by LSEG expect the division to hit an EBIT of 1.6 billion euros this year. On listed rival Haleon’s 15.6 times multiple, that business could be worth 25 billion euros. The rest of the Sanofi business may generate EBIT of 11.4 billion euros. Put that on a valuation multiple of 15.1 times 2023 EBIT – the average of rivals Roche, Novartis, Novo Nordisk, GSK and AstraZeneca – and that business could be worth 172 billion euros. Together, the two businesses could be worth 197 billion euros. That’s a healthy 76% above Sanofi’s current market capitalisation. The problem is that investors don’t appear to want to take the harsh medicine that leads to a cure. (By Karen Kwok)

(Source: Reuters Breakingviews)

Advertisement

17:01 IST, October 29th 2023