Published 22:28 IST, May 1st 2024

Lenders such as Austria’s Raiffeisen Bank International (RBI) and Italy’s UniCredit still have a sizable business in the country.

Advertisement

Russian roulette. For European banks, having a Russian presence is becoming an intractable problem. Two years after the invasion of Ukraine, lenders such as Austria’s Raiffeisen Bank International (RBI) and Italy’s UniCredit still have a sizable business in the country. Fearing lack of scrutiny in a sanctions-hit nation, the European Central Bank is ratcheting up the pressure. A costly exit looks preferable to possible penalties.

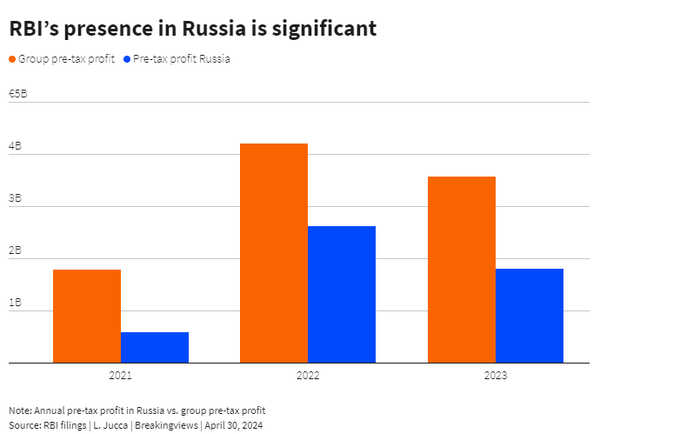

While Société Générale opted to quickly sell its Russian business at a discount in 2022, others including OTP Bank and ING have maintained operations in the country. Pre-tax profit at RBI’s Moscow-headquartered local subsidiary jumped to 1.8 billion euros in 2023 from nearly 600 million euros in 2021, representing about half of the group’s total last year. At UniCredit, Russian pre-tax profit hit nearly 900 million euros in 2023, triple its pre-war level, though the country represented just 8% of the group total. Rising earnings happened even as both lenders worked to shrink their local business. Euro zone banks’ activity in Russia has declined by 50% since the start of the war, reckons ECB supervision boss Claudia Buch.

Advertisement

European regulators have however grown frustrated with the situation. First, Russian subsidiaries of Western banks must pay taxes to Moscow, which the Financial Times estimated at 800 million euros in 2023. This risks helping finance the offensive against Ukraine, although the overall contribution would be tiny. Secondly, EU banks’ central offices may not be able to carry out in-depth scrutiny of business operations in Russia, potentially exposing themselves to a breach of European or, worse, U.S. sanctions.

These concerns have prompted the ECB to order in April that RBI slash its loans to customers in Russia. Frankfurt is set to pressure UniCredit to also pare back activities in the country, Reuters has reported citing people with knowledge of the discussions. Failure to comply would risk daily fines of up to 5% of the bank’s daily turnover and possibly other sanctions.

Advertisement

For the holdouts, the time to find a viable exit strategy from Russia, like a sale, seems to be over. The Kremlin may also decide to nationalise Western banks. Faced with such unappealing options, it’s probably time to consider a full withdrawal. UniCredit estimates the hit from what it calls an “extreme loss scenario” in Russia at 3.1 billion euros. That’s equivalent to just 37 basis points of its common equity Tier 1 capital, and would leave UniCredit with a healthy ratio of 15.5% – manageable even with the loss of future income.

RBI would find it much trickier to disentangle itself. A Russian phase-out would shrink its CET1 ratio to 14.6% from just over 17%. But it would depress its income. Either way, as regulatory pressure increases, maintaining a banking foothold in Russia may not be worth it.

Advertisement

22:28 IST, May 1st 2024