Published 21:43 IST, May 7th 2024

European Central Bank President will almost certainly cut interest rates before the US Federal Reserve chief.

Advertisement

Odd couple. Christine Lagarde and Jerome Powell are about to consciously uncouple their monetary policies. The European Central Bank president will almost certainly cut interest rates before the U.S. Federal Reserve chief. Hardliners in Frankfurt worry divergence would hit the euro and import inflation. But the differences between the two economies mean contrasting monetary policies can live happily ever after.

Breaking up is famously hard to do, unless you are Gwyneth Paltrow. The American actress’s 2014 split from her pop star husband Chris Martin popularised the concept of “conscious uncoupling” as a more amicable form of divorce. Lagarde and Powell are about to test a central bank version of the concept.

Advertisement

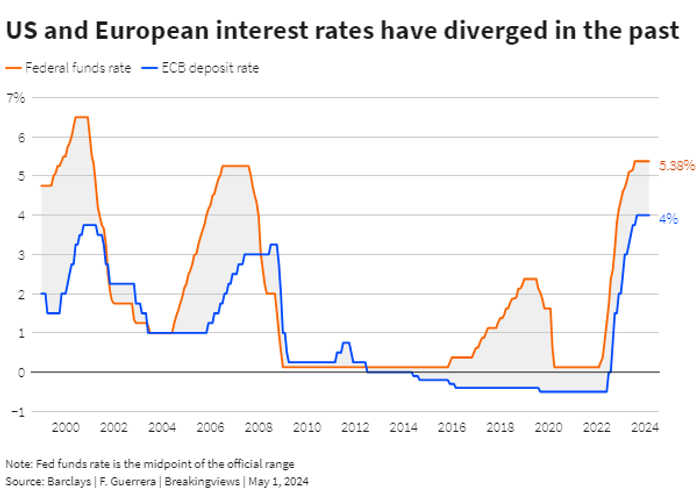

The two monetary authorities have diverged in the past. Indeed, between 2015 and 2019, the Fed hiked borrowing costs while the ECB reduced them below zero. But this would be the first time since the creation of the single currency that Frankfurt leads Washington when cutting rates.

In 2022 and 2023, the Fed and the ECB were joined in a marriage of convenience, increasing borrowing costs to slay rampant inflation. Now the ECB looks set to respond to sluggish growth and falling inflation next month by lowering borrowing costs for the first time since 2019, followed by up to two more cuts this year, according to investor expectations reflected in derivatives prices collected by LSEG. By contrast, markets expect Powell to reduce rates only once in 2024, because the U.S. economy is still expanding and inflation remains above the Fed’s 2% target.

Advertisement

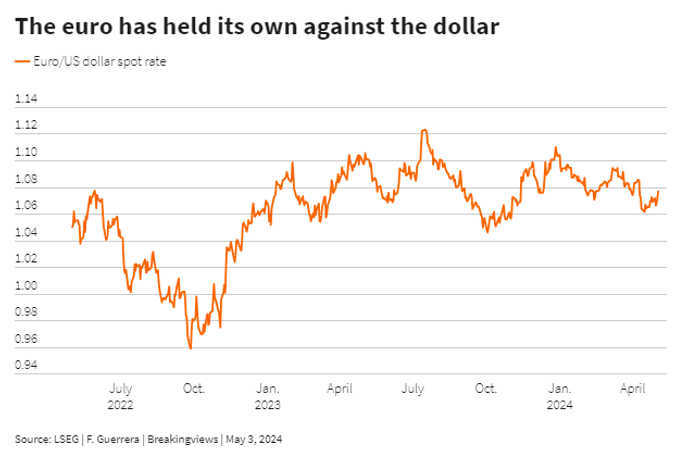

In that case, the difference between the benchmark interest rates in the euro zone and the United States could reach 2.1 percentage points, according to forecasts by Barclays analysts, compared with 1.4 percentage points today. The promise of higher returns could lure investors to the U.S., boosting the value of the dollar against the euro. In part, that’s already happening: the single currency has lost nearly 2.5% against the greenback since January.

The prospect of diverging rates is causing tensions inside the ECB. In April, Vice President Luis de Guindos told Le Monde that rate-setters would “need to take the impact of exchange rate movements into account.” In an interview with Bloomberg last month Robert Holzmann, Austria’s representative on the ECB’s Governing Council, said he would “find it difficult” to move too far away from the Fed. Yet Bank of Italy Governor Fabio Panetta argued that high U.S. rates would “reinforce the case for a rate cut”. And Lagarde recently stressed that the ECB is “data dependent”, not “Fed dependent.”

Advertisement

The main fear inside the ECB’s headquarters is that parting ways with the Fed could rekindle inflation by increasing the costs of imports. In practice, though, the euro zone is fairly insulated against this type of inflation and could even benefit from a cheaper currency.

For a start, the euro is not that weak: the single currency is still 13% higher than its low in September 2022, when one euro bought less than one dollar. And investors appear to have priced in some future divergence in interest rates. If the Fed delays easing policy until the first quarter of 2025, and the ECB cuts rates four times in that period, the euro will only fall an extra 1.2% against the dollar, according to Oxford Economics.

Advertisement

The effect on inflation would be negligible. ECB researchers found that a 1% depreciation of the euro would raise total import prices by just 0.3% within a year, while the upward pressure on headline inflation would be miniscule 0.04%. The limited impact is partly because some 40% of European imports are denominated in euros and therefore unaffected by exchange rate fluctuations.

Of course, a big jump in the costs of imported goods and services would have a more significant impact on inflation. That’s what happened between the beginning of 2022 and the first quarter of 2023, when Russia’s invasion of Ukraine pushed up energy and food costs. Higher import prices accounted for around two-fifths of euro zone inflation, according to an International Monetary Fund study. But that shock has abated. The ECB estimates the import deflator, a measure of import prices, will fall by 0.4% this year after dropping 3% in 2023.

Advertisement

A weaker euro also has some benefits for the bloc’s producers. Since the middle of last year, sluggish exports have dragged on euro zone growth as demand from large markets such as China slowed down. A cheaper currency would make BMW cars and Italian parmesan cheese more attractive for overseas buyers. The ECB expects foreign demand for euro zone products to rise by 2.4% this year and 3.1% in 2025, more than three times the rate than in 2023.

Of course, European rate-setters cannot relax entirely. Research by American University’s Valentina Bruno and Hyun Song Shin of the Bank for International Settlements shows that a rise in the dollar makes world trade harder and more expensive. Moreover, higher rates in the United States can spill over to other countries because other government bond markets tend to take their cue from U.S. Treasury yields.

Two further unpleasant surprises could turn the amicable divorce between the ECB and Fed into a messy affair. The first would be another surge in energy prices, most likely caused by the current turmoil in the Middle East. For the moment, however, oil prices are around $82 a barrel, well below the $120 they reached in 2022. The second would be if the Fed decided it was necessary to raise interest rates. At present, markets believe Powell has merely delayed rate cuts and will start to ease policy when inflation slows down. Yet stubborn prices and persistent economic growth might force the Fed to rethink. That would almost certainly push the dollar higher, sending shudders through foreign exchange markets from Europe to Japan.

Either of those two scenarios could prompt the ECB to rethink its rate-cutting strategy, causing currency gyrations, unsettling capital markets, and weighing on growth. For now, however, the ECB and the Fed can go their separate ways and experience a world where, as Paltrow put it, they can “break up and not lose everything”.

21:43 IST, May 7th 2024