Published 11:26 IST, March 25th 2024

The money manager argues Australia’s bourse is a better home for miners than its UK counterpart.

Advertisement

Trading places. Moving Down Under often appeals to northern Europeans seeking better weather, barbecues and beaches. Now a Sydney-based hedge fund is trying to persuade Glencore there’s another reason to decamp: a juicy valuation boost if the mining-cum-trading firm switches its listing from London to the Australian Stock Exchange. Tribeca Investment Partners makes an enticing case, but one that’s ultimately a chimera.

The money manager argues Australia’s bourse is a better home for miners than its UK counterpart as it hosts more of them and at higher multiples because investors there are more “pragmatic” about the continuing role of coal and other fossil fuels in the energy transition.

Advertisement

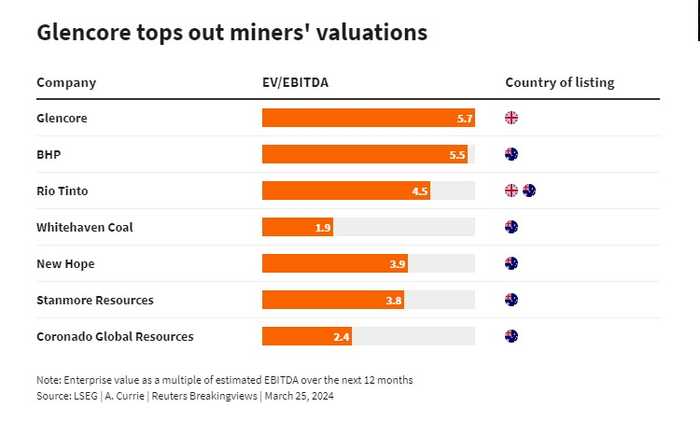

Throw in the country’s large, fast-growing pension – or superannuation - funds and tax breaks on dividends, and the demand to own the $65 billion company run by Gery Nagle would add between 30% and 100% to its current valuation, thereby generating a significant premium not just to its London valuation, but to peers like BHP and Rio Tinto, according to Tribeca.

Yet the super funds are not consistent big owners of fossil fuel-focused extractors or metals-heavy players like BHP. So there’s no reason they’d jump into an ASX-listed Glencore.

Advertisement

Moreover, Tribeca’s argument rests on Glencore keeping all its coal assets, contrary to the group's aim to spin them out after completing its acquisition of 77% of Teck Resources’ coking coal business. Were Nagle to reverse course and retain them, it would undermine Tribeca’s comparison with BHP, which has sold most of its fossil-fuel businesses.

Arguably, a coal-heavy Glencore should be saddled with a lower valuation, even on the ASX. The average enterprise of Aussie coal companies like New Hope and Stanmore Resources trades at 3 times EBITDA for the next 12 months. That, Tribeca points out, is an 88% improvement in a year and in line with the industry’s 10-year average.

Advertisement

But it’s way short of the roughly 6 times multiple Glencore sports. So for Tribeca’s idea to pan out, shareholders would have to ascribe an unprecedentedly high multiple to at least one of the miner’s three core businesses: coal, which accounts for more than half of revenue; its copper, cobalt and nickel operations; or its trading unit, whose leverage and funding needs contribute to Glencore’s cost of capital breaching 10%, compared with less than 8% at BHP, per LSEG data.

That seems unlikely regardless of where Glencore's stock trades, leaving Nagle free to limit any thoughts of Australia's sunny climes to daydreams.

Advertisement

11:26 IST, March 25th 2024