Published 20:19 IST, April 15th 2024

From the perspective of Western investment bankers dying to get a cut of the Gulf petrodollar boom, FAB seems to be sitting on a goldmine.

Advertisement

Not a FAB idea. First Abu Dhabi Bank seems to have the M&A bug. After a short-lived pursuit of London-listed Standard Chartered last year, the $40 billion Gulf lender has recently been eyeing possible targets in Turkey, Bloomberg reported. FAB Chief Executive Hana al-Rostamani has some good reasons to do so, but she’d be better off growing slowly at home instead.

From the perspective of Western investment bankers dying to get a cut of the Gulf petrodollar boom, FAB seems to be sitting on a goldmine. It has deep links into local energy giants like Abu Dhabi National Oil Company and cash-rich sovereign wealth funds like Mubadala Investment Company, which is also its largest shareholder with about two-fifths of the stock.

Advertisement

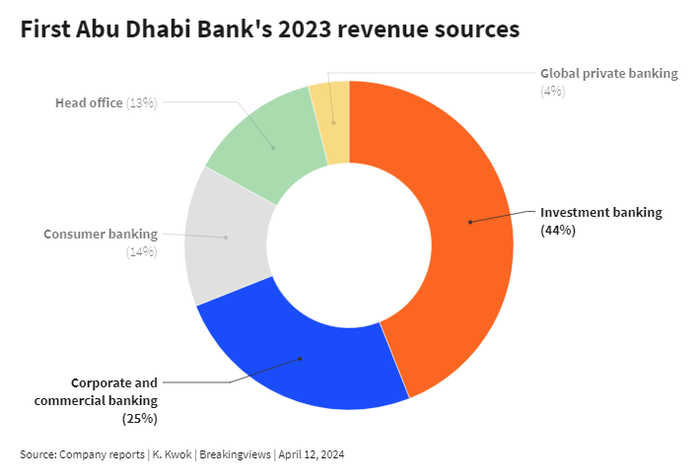

The downside, which may partly explain al-Rostamani’s apparent dealmaking zeal, is that FAB looks lopsided. More than two-thirds of its revenue came from the typically volatile divisions of corporate and investment banking last year, while it does relatively little of the traditional banking business of lending out deposits. It’s also overwhelmingly dependent on its home market, whose fortunes tend to rise and fall with the oil price.

One way to build a more balanced bank would be to do a deal in the United Arab Emirates. But smaller lenders wouldn’t be big enough to move the needle. Meanwhile, clubbing with other UAE-based banks in Dubai, like $30 billion Emirates NBD, looks impossible: the respective royal families would be reluctant to lose control of their home lender.

Advertisement

Hence FAB’s overseas interest. Al-Rostamani’s corporate customers are typically government-linked entities, who export energy to fast-growing economies in Asia and the Middle East. Buying a bank like StanChart, which does a lot of business in these markets, could allow al-Rostamani to cross-sell products. She’d also get her hands on a collection of retail deposit-focused franchises, lowering FAB’s funding costs. A similar logic, though on a smaller scale, applies to the Turkish interest: trade flows between the country and the UAE have soared.

The problem, however, is that cross-border tie-ups tend to be light on concrete cost savings. That means FAB might not have a sound justification for offering a premium over the target’s share price. Nor is it obvious that al-Rostamani could pay in cash: FAB’s common equity Tier 1 ratio of 13.8% is just above her target of 13.5%, giving her minimal wiggle room. The upshot is that she’d have to pay in shares, which is probably unpalatable for foreign targets’ investors, or call on Mubadala for cash.

Advertisement

It might be simpler to grow at home instead. Lending in the consumer-banking business rose by 9% last year, compared with 1% and 7% respectively for corporate and investment banking. That suggests there’s room for al-Rostamani to re-balance the units slowly over time. It might be less fun than a flashy deal, but it would also be less scary for shareholders.

Context News

First Abu Dhabi Bank is studying potential acquisition targets in Turkey, including Yapi Kredi, Bloomberg reported on April 5 citing people familiar with the matter.

Advertisement

20:19 IST, April 15th 2024