Published 14:04 IST, April 13th 2024

JPMorgan and rivals Citigroup and Wells Fargo reported first-quarter earnings on Friday, and all did better than analysts polled by LSEG had expected.

Advertisement

Constructive ambiguity. There’s a big difference between preparing for the worst and expecting it. For investors in U.S. banks, divining that difference is an exercise in frustration. Take JPMorgan, where boss Jamie Dimon is avoiding being pinned down on where the economy is heading, despite warnings that grim times may be ahead. It’s smart to plan for all eventualities. The catch is that it adds volatility where investors aren’t used to it.

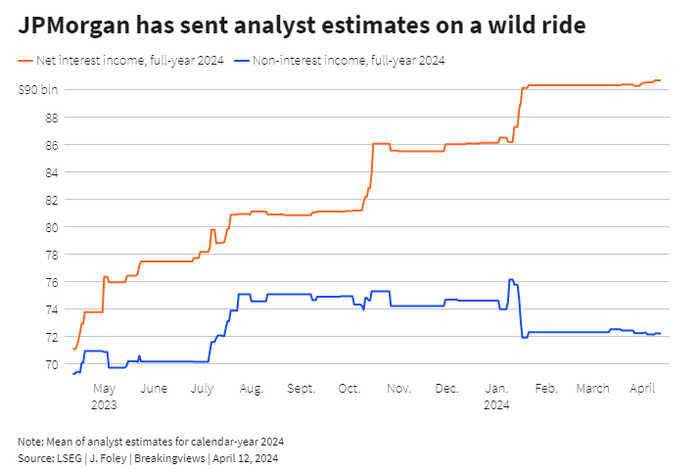

JPMorgan and rivals Citigroup and Wells Fargo reported first-quarter earnings on Friday, and all did better than analysts polled by LSEG had expected. Yet on one measure of future performance, they disappointed. All three left their full-year estimates of interest income – the largest component of revenue – substantially unchanged. That’s despite the benefit big lenders ought to get from diminishing expectations of interest-rate cuts from the U.S. Federal Reserve. JPMorgan’s shares fell nearly 6% in early trading.

Advertisement

Dimon rationalizes that no one actually knows where rates will go, saying on Friday’s earnings call that consensus views “have always been wrong.” Wells Fargo boss CEO Charlie Scharf walked a similar line on the danger of predicting. His bank is basing guidance on three expected cuts in 2024, despite bond investors now seeing two cuts as more likely.

The trouble is that these assumptions can have a huge impact on interest income, which is supposed to be more stable than uncertain businesses like trading and investment banking. A year ago, analysts thought JPMorgan would make around $70 billion of net interest income in 2024. That forecast is now $90 billion. By comparison, analysts only nudged estimates of non-interest income from $69 billion up to $72 billion.

Advertisement

Wall Street leaders have little to gain from prognosticating on rates, either in word or deed. Consider Bank of America, which plowed $600 billion into mortgage bonds that plunged in value as rates rose, resulting in a theoretical loss of nearly $100 billion at 2023’s end.

Besides, over the long run, the vagaries of the next few months should matter less than consistently rolling with the punches. That’s one reason JPMorgan trades at 2.4 times its tangible book value, according to LSEG, triple the valuation of Citi and its shifting strategies. Investors want direction – and on some topics, like politics and regulation, Dimon still doles it out. On others, he’s right to preserve the mystery.

Advertisement

Context News

JPMorgan reported $13.4 billion of earnings for the first quarter of 2024, a 6% increase on the same period a year earlier. Nonetheless, the shares fell more than 5% in early trading on April 12 after the U.S. lender left its expectations for interest income broadly unchanged at $89 billion for the year, excluding contributions from its trading business. It had previously forecast $88 billion. Citigroup and Wells Fargo also reported earnings on April 12. Both left their guidance for interest income unchanged. Bond investors have been pricing in a sustained period of elevated U.S. interest rates, as consumer price data has shown inflation stubbornly sticking above the Federal Reserve’s 2% target.

14:04 IST, April 13th 2024