Published 18:10 IST, April 17th 2024

After two post-Covid boom years, the French behemoth and its bling peers are facing a phase of revenue stagnation.

Advertisement

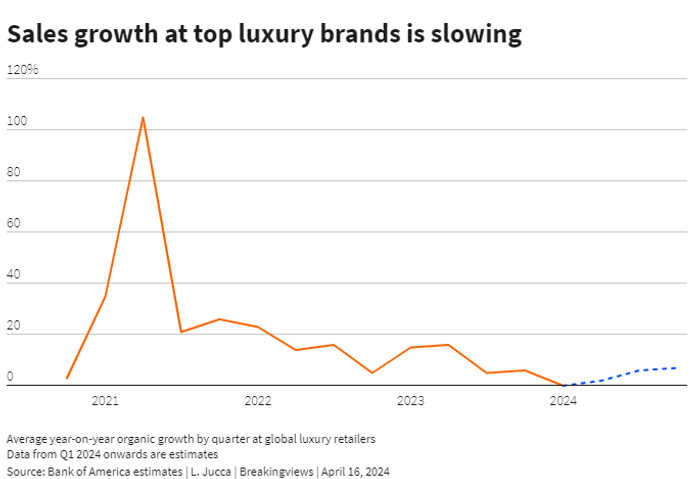

Growing apart. The world of luxury is increasingly a tale of the haves and the have-nots. Bernard Arnault’s $420 billion Tiffany-to-Dior conglomerate LVMH sent a sobering message on Tuesday as it unveiled a 3% year-on-year rise in first-quarter sales ignoring currency moves – well below the 13% expansion for 2023 as a whole. After two post-Covid boom years, the French behemoth and its bling peers are facing a phase of revenue stagnation. As growth flattens, a pre-existing gap between winners and losers may widen.

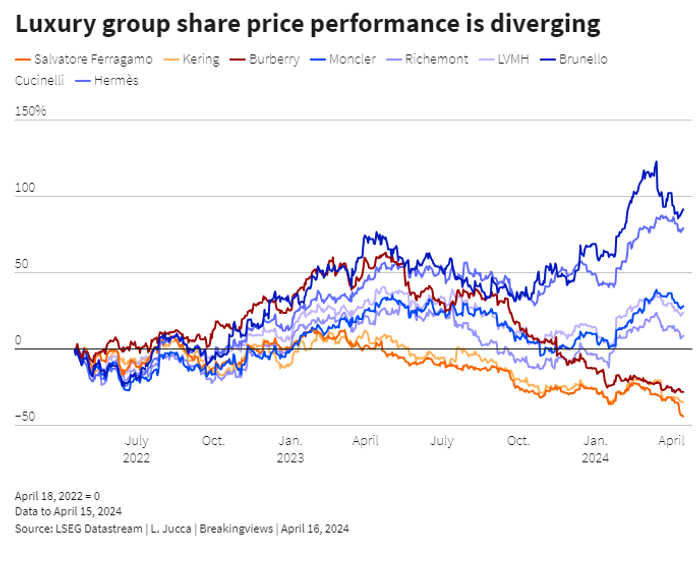

Investing in European luxury used to be a one-way bet. Considered defensive due to their supposedly more resilient customer base, these stocks tended to attract investors even in times of crisis. Shares in LVMH, for instance, rose 50% between 2007 and 2012 even as the aftermath of the global financial crisis prompted a 35% fall in the STOXX Europe 600 Index, LSEG data show. In the following decade, LVMH rose 450% compared to a rise in the European stock market benchmark of only 80%.

Advertisement

The past few months show a different trend. Rising inflation and a slowdown in China, which together with other Asia-Pacific markets represents around 40% of global luxury sales, have eaten into shoppers’ purchasing power. But the impact has been uneven. While ultra-luxury brands like $255 billion Birkin bag purveyor Hermès International and $7 billion “king of cashmere” Brunello Cucinelli continued to attract buyers, more challenged brands like Kering’s Gucci, Burberry and Salvatore Ferragamo – which rely on less affluent shoppers and are trying to reinvent themselves with new designers – have struggled to woo shoppers.

LVMH, which also sells jewellery and wine and whose top brand Louis Vuitton shares exclusivity traits with Hermès, should continue to be classed as a winner despite its pedestrian first quarter. But for the luxury sector as a whole, like-for-like revenue is on average expected to stay flat in the first quarter, the worst quarterly performance since the end of 2020, and rise just 2% in the next, Bank of America estimates show. That suggests the sector’s sales growth could be half the 9% or so recorded last year and way off the double-digit expansion seen in 2022. With less growth to go round, the overall numbers may hide some markedly different trajectories. While Cucinelli sales are forecast to jump 13% this quarter, Burberry’s are seen slumping 12%, according to Visible Alpha estimates.

Advertisement

Some of these considerations have started to feed into luxury stock prices: Burberry and Ferragamo shares are down around 20% since the start of the year, Hermès is up 20%, while LVMH lies in between, up 8%. The polarisation is unlikely to disappear: Gucci’s struggles suggest brand name alone is no guarantee of eternal success. The risk is that some famous designers end up in the bargain bin.

18:10 IST, April 17th 2024