Published 14:17 IST, February 22nd 2024

Chipmaker Nvidia on Feb. 21 reported about $22 billion of revenue for the quarter ending Jan. 28, a 265% increase from the same period a year earlier.

Advertisement

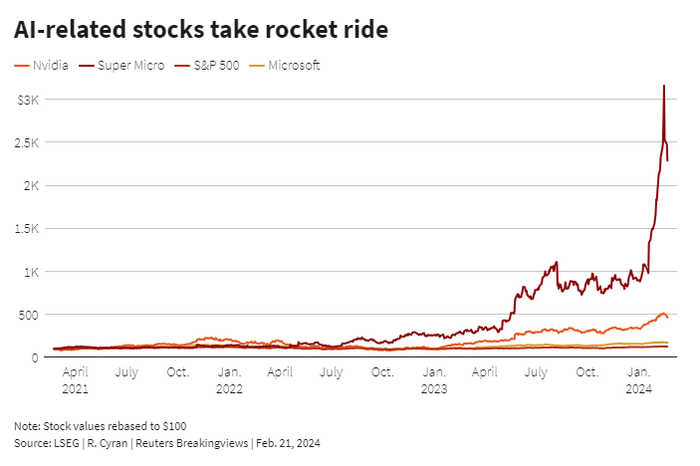

Blue sky’s the limit. Nvidia’s astonishing rise has further to go. Unlike other dubious beneficiaries of artificial intelligence hype, the $1.7 trillion chipmaker’s piece of the market will be hard to pry away. It could soon be worth nearly twice as much again.

Although the company is now forecasting much slower growth, its top line surged 265% in the three months ending Jan. 28 from a year earlier, it said on Wednesday. Its earnings per share have grown nearly nine times over the span, supporting the frenzy behind a tripling of its stock price over the past 12 months. Nvidia’s circuitry, which dominates the market for training AI systems, is in high demand as technology titans race to build data centers.

Advertisement

There’s no shortage of mania either. Super Micro Computer, whose shares have soared 750% since last February, concedes that barriers to entry are low in its business of building computer servers. Its gross margin, or revenue less the primary costs of production, clocks in at a paltry 18%.

By contrast, Nvidia looks like the real deal. It spends a chunky 11% of sales on R&D to sustain its stronghold, and a 76% gross margin indicates considerable pricing power. It even pays a dividend, which suggests that founder Jensen Huang is carefully allocating capital.

Advertisement

These advantages are significant. Lisa Su, the boss of rival AMD,

It’s a plausible outlook. One way to get there would be a quadrupling of AI users to 800 million, their daily usage quintupling, chips improving at historic rates and AI model complexity only tripling annually instead of today’s 10-fold rate, according to New Street analysts. The increase in users would mirror the internet’s expansion from 1999 to 2003, and estimates each person only uses 15 minutes of full AI server time per day.

Advertisement

Nvidia is in prime position to take advantage. If it claimed 75% of that market and assuming, for simplicity’s sake, that its other businesses didn’t grow, it would lead to about $325 billion of revenue, approximately 50% more than Microsoft’s last fiscal year and half as much as Walmart’s. At a 30% net profit margin, far less than what it generates now, on the same 35 times multiple of earnings where it has traded over the past decade, Nvidia would be worth $3.4 trillion. Competitors will be gunning for it and AI’s promise could fall short, but the thesis is anything but artificial.

(This story has been corrected to add the dropped word "trillion" in the first paragraph.)

Advertisement

Context News

Chipmaker Nvidia on Feb. 21 reported about $22 billion of revenue for the quarter ending Jan. 28, a 265% increase from the same period a year earlier. The company earned $4.93 per share during the three-month period, compared to 57 cents a year ago. Nvidia said it expects revenue in the current quarter to be $24 billion, plus or minus 2%.

14:17 IST, February 22nd 2024