Published 20:44 IST, March 18th 2024

Putin boasts that Russia grew 3.6% last year, more than any of the Group of Seven rich democracies which are backing Ukraine.

Advertisement

It’s the oil, stupid. Vladimir Putin is winning the war of attrition against Ukraine. Although the Russian people are also suffering, the pain is not enough to force the newly re-elected president to change course. He might reconsider if the West could squeeze Russia’s oil revenue. But that will be hard to engineer.

Even if receipts from hydrocarbons stay at the same level, the Russian government is going to have to squeeze its citizens. The economy is overheating as Putin, who has just secured a new six-year term to extend his 24-year rule, pumps more money into the war effort. Defence spending, which is budgeted at 10.8 trillion roubles ($118 billion) this year, has trebled since the war began. Inflation is 7.7% and there are severe labour shortages.

Advertisement

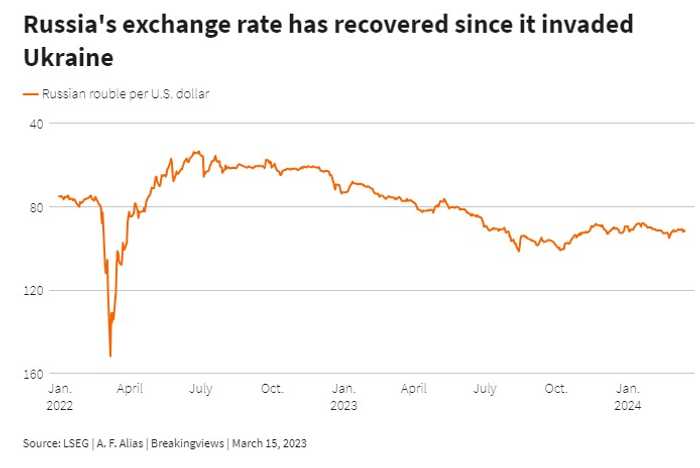

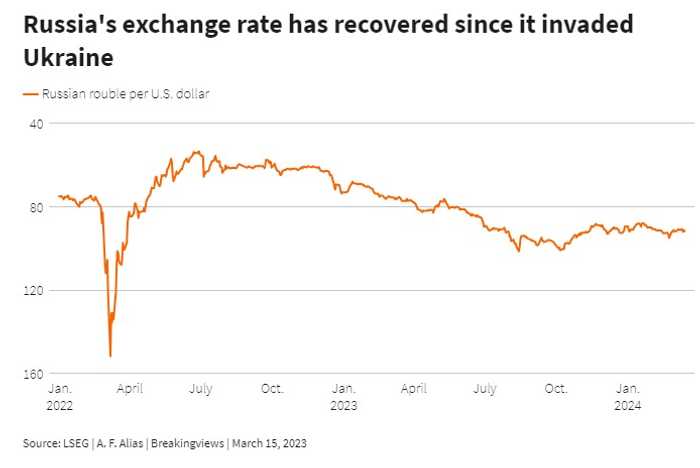

The central bank has jacked up interest rates to 16% and said official borrowing costs will need to stay high for a “long period” to get inflation down to its 4% target. The government has imposed capital controls to prop up the rouble.

The government will also need to take fiscal measures to bring domestic consumption in line with production. Top of the list are likely to be tax increases focussed on richer individuals and companies. Putin has already signalled as much. While such decisions will be unpopular with some, he will face no opposition ramming them through.

Advertisement

Guns versus butter

Putin boasts that Russia grew 3.6% last year, more than any of the Group of Seven rich democracies which are backing Ukraine. It will grow 2.6% this year and 1.1% next year, the International Monetary Fund predicts.

But the underlying picture is not as healthy as these headline figures suggest. For a start, a war economy by its nature does not produce goods that ordinary people can consume. As the government directs a bigger slice of national income into churning out tanks and shells, there will be less money for consumer goods and services, says Tim Ash, a strategist at RBC BlueBay Asset Management.

Advertisement

The government has shielded the population from the economic cost of the war by raiding its national wealth fund to finance the budget deficit, which was 3.7% of GDP last year. But this is not sustainable as the fund’s liquid assets have fallen by more than half since the Putin invaded Ukraine two years ago, and are now just 2.7% of national income. One way or another, the war economy will crowd out non-war spending. This will happen through a mixture of tax hikes, inflation, high interest rates and spending cuts.

What’s more, the war is hurting Russia’s mid-term prospects. Western sanctions are denying it advanced technology. Labour productivity, which Putin dreams of boosting, fell 3.6% in the first year of the war. Investment dropped to 19.7% of GDP in 2022, from 21.4% in 2017.

Advertisement

About 315,000 Russian troops have died or been injured, according to the U.S. government, while Re: Russia, an independent publication, estimates over 800,000 people had fled the country by last July. This brain drain of young and educated people is a further drag on the economy.

Russian roulette

Although the economy seems likely to stagnate, the president does not face any domestic financial constraint to prolonging the war. Nor is he yet under any external restrictions.

Advertisement

Putin has been able to sustain the invasion because Russia is still earning a lot from hydrocarbons. Despite Ukraine’s allies embargoing its oil and Europe finding alternatives to its gas, Russia enjoyed a current account surplus of $51 billion in 2023. Though that was down from a bumper $238 billion the previous year, Moscow is still in the black.

Things might change if Ukraine’s allies could drive Russia’s export revenues down so far that it goes into deficit, says Jacob Nell, a senior research fellow at the Kyiv School of Economics. He argues that Russia, and the Soviet Union before it, faced crises when the current account went into the red.

Because Russia could shrink imports a bit, if necessary, Nell estimates that exports would have to fall by about $80 billion before Putin had to take extreme measures to stabilise the economy. About $30 billion of that could come from a tighter gas embargo plus restrictions on exports of fertilisers and metals such as nickel. But the bulk would have to come from cutting the price Moscow receives for its oil to $50 a barrel.

This is easier said than done. The G7 and other allies imposed a price cap of $60 a barrel on Russian oil in late 2022. However, Urals crude is trading at around $71 per barrel, about $14 below the Brent variety. Although the United States has tightened up sanctions on tankers that bust the price cap, Russia can partly evade them by using its own fleet.

Ukraine’s allies could get lucky if the global oil price plummeted. Without that, they will need much tougher measures to drive the price Russia receives for its oil down to $60, let alone $50.

Key to achieving that will be to persuade India, the largest importer of Russian seaborne oil, to stop paying more than the price cap, says Nell. The country might then benefit from cheaper oil — and its refiners might increase their profits.

The problem is that Russia might refuse to sell crude at such low prices and, instead, curb production. That would push up the global oil price — which would hurt India as well as Ukraine’s allies. Though cutting oil shipments would hurt Russia, Putin might be willing to take the risk for a while if high oil prices would increase the chance of Donald Trump winning November’s U.S. presidential election.

Ukraine’s allies are not yet willing to take the necessary risks to crush Russia’s revenues. Until they do, there is no financial reason for Putin to stop fighting.

20:44 IST, March 18th 2024