Tata Trust Trustee Venu Srinivasan Resigns From Bai Hira Bai Trust

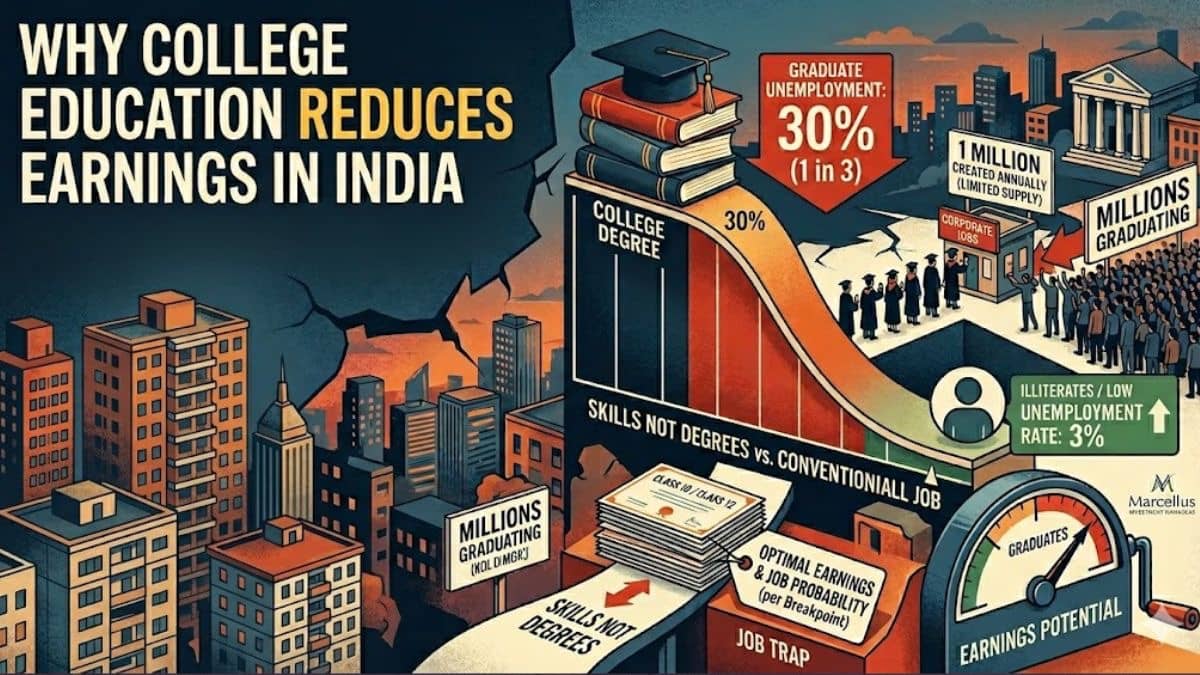

Why College Degree Reduces Earnings In India - Marcellus CIO Weighs In

No More Sprinkles? Dunkin' Donuts To Shut Down In India; Know When?

Tata Steel Receives Rs 1,755 Cr Demand Notice Over Excess Coal Mining

Crude Oil Supplies Secured, No Payment Issues For Iran Imports: MoPNG