Published 17:26 IST, October 28th 2023

What purpose do bonds serve? Here's a deep dive.

Advertisement

Back from the dead. Last week, I was tasked with convincing a class of brilliant young MBA students at one of Europe’s leading business schools that they should consider a career in bond investing. It was not an easy sell.

Bonds, I explained, traditionally serve three purposes. First, they deliver a positive income. That prompted polite guffaws. I should not have been surprised. In 2022, the aggregate U.S. market for fixed income securities notched up its worst annual performance since 1871, and U.S. Treasury bonds are currently on track for three consecutive calendar years of negative returns – something that has never happened before.

Bonds contribute capital stability, I parried, in contrast to flighty equities. More sniggers at the back. I sensed familiarity with the recent fate of fixed income benchmarks such as Austria’s hundred-year government bond. That security, which was issued in 2017, is down around 75% from its peak valuation in late 2020.

Advertisement

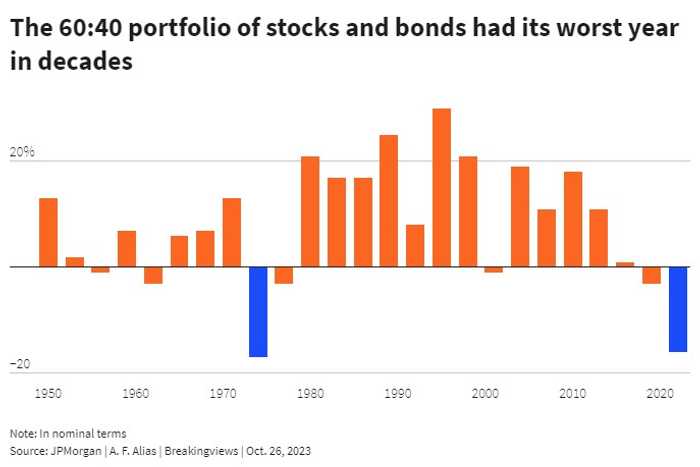

There was still fixed income’s trump card. Its third traditional function is as ballast: an asset class whose negative correlation with equities can diversify a portfolio and reduce overall risk without giving up returns. Then I remembered that in 2022 equities and bonds dropped in tandem, resulting in the worst performance for the classic 60:40 balanced portfolio since 1974.

The private equity session was about to start down the hall. Some of the more ambitious students were beginning to slink towards the door. It was time for a change of tack.

Advertisement

It is true, I admitted, that being a bond investor has been tough for much of the past 15 years and positively traumatic over the past two. But you should not choose your future career by looking in the rear-view mirror. The three fundamental drivers of fixed income returns that distinguish them from equities imply that the immediate future is likely to be very different from the past.

The first is interest-rate risk. That has certainly been a handicap for investors over the past two years as rising yields battered the market value of long bond positions.

Advertisement

Yet the result is that yields today are at far more attractive levels. The yield on nominal 10-year U.S. Treasury notes touched 5% this week, while their inflation-protected cousins are yielding 2.5%. This means even the plainest vanilla assets in the global system provide income sufficient to fund medium-term liabilities again.

That’s a welcome change on its own, but it comes with an even more important kicker. The income and capital payments on bonds are contractually fixed, unlike the cash flows provided by equities. For this reason, when bond yields are low, the sensitivity of capital prices to inflation and interest rate shocks is high, and vice versa. This critical property of fixed income securities – “convexity” in the jargon – means that as bonds sell off, their downside risk mechanically falls. That is quite a contrast to the dynamics affecting equity values.

Advertisement

Precisely because of the carnage of the past two years, the cushion of convexity already makes a material difference to the risk-reward ratio in global government bonds. And if current expectations for growth, inflation and policy interest rates turn out to be too bullish, its effect will swing into reverse: falling yields will deliver capital gains from rising bond prices at an accelerating pace. Don’t let anyone tell you that bond maths can’t be fun.

The second potential source of return in fixed income is credit – the reward for bearing the risk that the bond issuer defaults. The picture here is admittedly less clear-cut. While underlying government yield curves have adjusted materially, many credit spreads have moved much less.

Advertisement

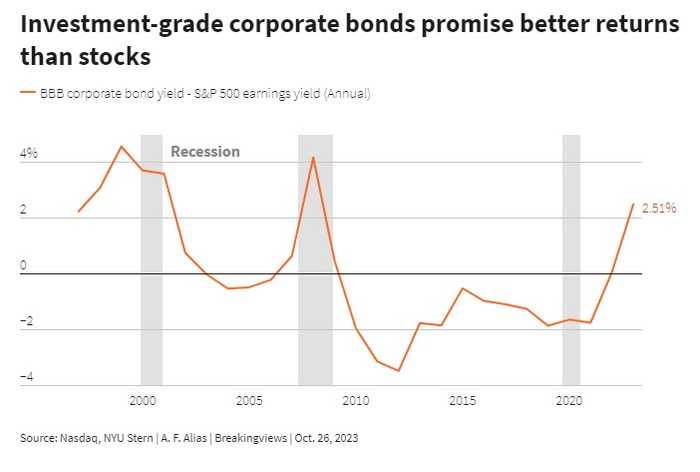

Nevertheless Torsten Slok, chief economist at Apollo Global Management, points out that the upward shift in the U.S. Treasury curve alone means that the yield on BBB-rated U.S. corporate bonds is now two and a half percentage points higher than the earnings yield of the S&P 500. Since the latter metric measures the totality of profits available for distribution to shareholders, that suggests bonds issued by investment-grade U.S. companies are now better value than their equities, after more than a decade in their shadow.

In more esoteric parts of the global credit universe, valuations now look healthy in absolute terms as well. The U.S. dollar-denominated bonds of emerging-market governments are a case in point. The yield of the benchmark JPMorgan EMBI-GD index is close to 4.5% above U.S. Treasuries. But fund manager GMO’s emerging debt team calculates that recent ratings upgrades imply expected credit losses of only one third of that differential. If historical averages prove a reliable guide, that suggests an annualised return for emerging-market sovereign debt of nearly 5% over U.S. Treasuries over the coming two years.

For those brave enough to make event-driven bets on today’s chaotic geopolitical environment, potentially greater opportunities await. Look no further than Venezuela for proof. After the U.S. eased sanctions last week, its dollar-denominated bonds nearly doubled in price.

Finally, there is the third engine of returns for global fixed income investors: currency risk. No one would pretend this is a game for the faint-hearted – or that valuation alone is a sure-fire route to success. Yet it is hard to ignore that of 54 global currencies monitored by the Economist for its Big Mac index, all but seven are currently cheap when compared to the U.S. dollar. The appreciating greenback has been a drag on much of the global fixed income universe for the past decade. Positioning for a reversal could be the trade of the next one.

My tirade had stemmed the outflow of students. It was time to go in for the kill. The real reason to go into fixed income investing, I explained, is that you get to tell governments what to do. The rapid fall of UK Prime Minister Liz Truss just over a year ago showed the “bond vigilantes” are back.

It has been three decades since U.S. President Bill Clinton’s campaign supremo, James Carville, said he’d like to be reincarnated as the bond market, because then he could intimidate everybody. Now that the end of monetary anaesthesia has awoken fixed income from its 15-year coma, I told the MBA students, you’ve got your chance.

17:26 IST, October 28th 2023