Published 19:23 IST, April 24th 2024

The IMF predicts that world GDP will expand by 3.2% both this year and next, the same pace as in 2023.

Advertisement

American beauty. The United States is the MVP of GDP. That was the International Monetary Fund’s verdict at its spring gathering last week. The U.S. star turn is much needed as other key members of the global growth team, like Europe and China, are lagging. But its performance has been fueled by worryingly high debt and one-off gains in productivity and the workforce. In the long run, even this extraordinary athlete may run out of puff.

As central bankers and finance ministers arrived for the semi-annual event organized by the IMF and the World Bank, Washington’s famous cherry trees were already shedding their flowers. It was an apt metaphor: Wars, trade tensions and high interest rates have taken the bloom off the global economy.

Advertisement

Sure, the IMF predicts that world GDP will expand by 3.2% both this year and next – the same pace as in 2023. But that’s below the 3.8% annual average the global economy managed between 2000 and 2019. By 2029 the IMF expects growth to be just 3.1%, the lowest rate in decades.

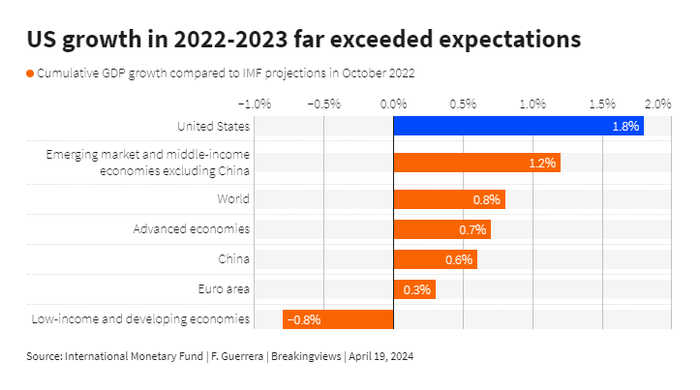

Without the United States, results could have been even worse. After growing by 2.5% last year – a pace matched only by Spain among advanced countries – the world’s biggest economy will expand by 2.7% in 2024, the IMF projects. That’s more than three times faster than the euro zone.

Advertisement

China, the other reliable recent contributor to global GDP, is also limping. Growth there will slow from 5.2% last year to 4.6% in 2024 and 4.1% in 2025, the IMF reckons. “One growth engine is better than none,” a glass-half-full policymaker noted in the IMF’s cavernous headquarters. But what if that engine sputters?

A closer look at the U.S. economy’s vital statistics suggests there’s a danger of fatigue. The Covid tragedy prompted the federal government to unleash huge stimulus that equaled around 27% of GDP in 2020-2021, according to the Tax Foundation. It worked: Fiscal help boosted GDP growth by nearly 14 percentage points in the second quarter of 2020 alone, Brookings’ Hutchins Center calculates. And it left households with $2.1 trillion of excess savings above the pre-pandemic trend, according to the San Francisco Federal Reserve.

Advertisement

The pandemic stressed Uncle Sam’s balance sheet, though. The U.S. budget deficit went from 5.8% of GDP in 2019 to nearly 14% in 2020 and more than 11% in 2021. And the government continues to spend. The IMF estimates the deficit will average nearly 6.5% of domestic output each year until 2029 – almost double its level in 2015. American consumers have also continued to splash out. Last year, they spent 2.2% more than in 2022, above the 1.7% average growth between 2006 and 2015, the IMF reckons. In the euro zone, private consumer expenditure only expanded by 0.5% last year.

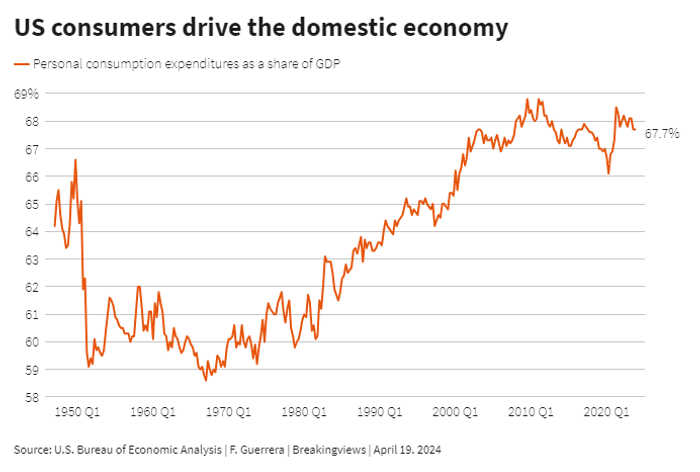

Since consumption accounts for nearly 70% of U.S. GDP, the vitality of American consumers is crucial to economic performance. They may be flagging, though. Excess savings have dwindled to $30 billion, while consumers are maxing out their credit cards. At the end of last year, 9.7% of card balances had not been paid for 90 days – the highest level since early 2021 – according to New York Federal Reserve data. Higher mortgage rates are scaring off buyers, with home sales falling 4.3% in March.

Advertisement

Low unemployment, decent wage growth and investment gains from the strong stock market may prolong the U.S. spending spree for a while, but the IMF expects growth in private consumer expenditure to fall to 1.6% by 2025.

The U.S. economy’s staying power has surprised the IMF and other forecasters. This is partly down to two factors which have proved hard to model, and which may be difficult to sustain. The first is a surge in immigrants. In November, the Congressional Budget Office upgraded its estimate of net immigration into the U.S. from 1 million people to 3.3 million. The big jump, which was largely due to increased illegal immigration, probably boosted consumer spending and economic growth, according to economists Wendy Edelberg and Tara Watson from the Brookings Institution. It seems unlikely, though, that illegal aliens can keep arriving in droves: both President Joe Biden and his Republican opponent Donald Trump have vowed to curb immigration.

Advertisement

The other surprise is that American workers have proved unexpectedly productive. In the last three months of 2023, hourly output per worker rose by 3.2% on the previous quarter, official data showed. That pushed productivity up by 1.3% in 2023, partly reversing a 1.9% slump in 2022. Nobody seems to know what happened. The reactions of economists and policymakers last week included shrugged shoulders, blaming “squishy numbers”, and asking the interviewer what they thought.

More productive workers and firms can make the difference between boom and bust. IMF research found that a slowdown in the growth of total factor productivity – a measure of capital and labor efficiency – explains more than half of the deceleration in global growth since 2009. Yet even after the latest surge, growth in U.S. productivity is still below its long-term annual average of 2.1%.

The government in Washington may keep throwing money at the problem. On this point, Biden and Trump are not that far apart. “Both parties like to spend”, noted a U.S. policymaker. But it’s not entirely up to them. The U.S. fiscal position is already perilous – the CBO estimates that, as a percentage of GDP, the budget deficit in 2034 will be 65% higher than the average for the past 50 years. A sustained increase in borrowing could spark investors’ concerns about the ability of the United States to service its debt, pushing up long-term bond yields and interest payments.

The United States’ pre-eminent position in the global economy, the dollar’s role as the key currency in world trade, and strong appetite for U.S. debt by countries with huge savings surpluses have so far ensured Uncle Sam can borrow at will.

Still, as sports fans know, a star player can only carry the rest of the team for so long. The United States is in great form right now, but unless the world economy can rely on other players, it will have to lower its ambitions.

19:23 IST, April 24th 2024