Published 17:01 IST, October 31st 2023

McDonald's is succeeding globally with a 9% increase in sales, partly by offering smaller, affordable meals in struggling economies like China and Germany.

Advertisement

Happy place. McDonald’s status as the world’s go-to meal means it’s competing with an uneven global economy as much as any rivals. The ubiquitous $190 billion fast-food purveyor on Monday touted a 9% year-over-year increase in worldwide same-store sales for the third quarter. In places like the U.S., that was helped by menu price increases. But the Big Mac seller also talked up the release of smaller, more affordable meals in markets facing worse economic fortunes, like China and Germany. In the latter, its McSmart menu of smaller meals helped drive the 10th quarter of double-digit sales growth. The company run by Christopher Kempczinski is striking a delicate balance.

In the U.S., the cost of food away from home grew 6% over the year to September, according to the Bureau of Labor Statistics, outpacing now-moderating food-at-home inflation. On a call with analysts, Kempczinski said that economic pressures are hurting low-income customers. But growth among higher-income consumers and bigger average checks picked up the slack. Meanwhile, worldwide, executives pointed to issues like relatively higher inflation in Europe, hammering a mantra of “affordable” or “affordability” 15 times on the call. That McDonald’s can selectively grow prices or shrink its offerings while upping both sales and operating profit shows that it occupies a unique sweet spot, even as it grapples with a global economy running at varying speeds between and within countries. (By Sharon Lam)

Advertisement

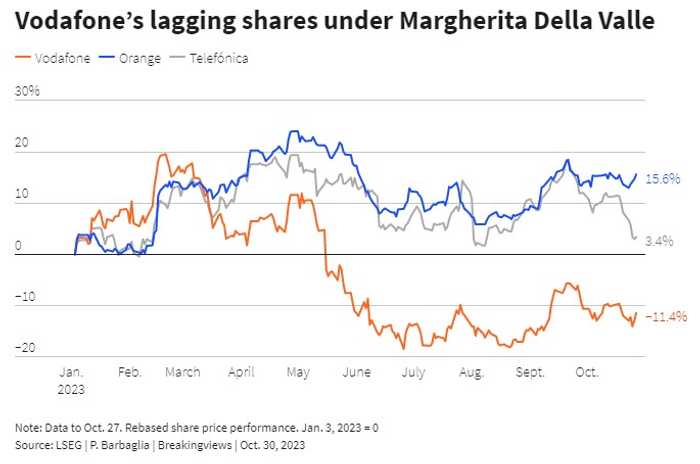

Mucho dolor. Vodafone’s boss Margherita Della Valle is cleaning up the sprawling 21 billion pound telecom group, but it’s a tough job. A potentially messy exit in Spain illustrates the point. Della Valle lacks an obvious partner in the country: local giant Telefónica is too big, while rivals Orange and MásMóvil are merging with one another. As a result, Vodafone may have found itself a potentially problematic counterparty for the Spanish business, which Della Valle has put under strategic review.

Zegona Communications, a London-listed cash shell run by former Virgin Media executive Eamonn O’Hare, is in talks to buy at least half of the Spain unit for an implied overall enterprise value of more than 5 billion euros, according to a Bloomberg report that cited people familiar with the matter. Local newspaper Expansión reported, citing market sources, that Zegona could buy all of the division’s equity – with the help of a debt package from Deutsche Bank, ING and UniCredit and a 900 million euro loan from Vodafone itself.

Advertisement

Both options could get messy. Tiny Zegona would have to borrow heavily to buy the whole thing, meaning it would be risky for Della Valle to remain exposed by lending to the buyer. A joint venture, meanwhile, would see a large chunk of the asset remain on Vodafone’s balance sheet until Zegona or another player could afford to buy it outright. That won’t help the parent group’s valuation much. Investors might be reassured that Della Valle is making things happen, but a clean break in Spain looks increasingly unlikely. (By Pamela Barbaglia)

Advertisement

Block deal. Lithium M&A is becoming a dangerous sport Down Under. On Friday, Hancock Prospecting, owned by Australia’s richest person Gina Rinehart, revealed it had snapped up an 18.3% stake in Azure Minerals. A day earlier her quarry, which is developing a project in Western Australia to mine the metal crucial for electric-vehicle batteries, agreed to a $1 billion takeover offer from the world’s second-largest lithium player, Chile’s SQM.

It’s the second time of late that Rinehart, whose wealth the Australian Financial Review pegs at some $24 billion, has intervened in a tie-up. The 19.9% stake she amassed in Liontown Resources made her the company’s largest shareholder and prompted suitor Albemarle two weeks ago to drop its $4.3 billion takeover.

Advertisement

SQM probably won’t cave as easily. Unlike Albemarle, it has not tied its hands by declaring the Azure bid to be its best and final offer. SQM also already owns 19.9% of its target and has secured the support of another 24% or so, per analysts at Canaccord.

Granted, the so-called scheme of arrangement method of buying an Australian company usually requires a buyer to secure backing from 75% of voting shareholders. But SQM boss Ricardo Ramos can switch to an off-market offer and try to buy other investors’ stakes first. Rinehart’s experience of scooping up shares, though, may give her the upper hand. (By Antony Currie)

Advertisement

17:01 IST, October 31st 2023