Published 14:23 IST, February 13th 2024

The buyer said on Monday it will pay $26 billion, including debt, for the private oil and gas company operating in the Permian Basin.

Advertisement

Separated at birth. Diamondback Energy is paying up for Endeavor Energy Resources because it can. The buyer said on Monday it will pay $26 billion, including debt, for the private oil and gas company operating in the Permian Basin. The two firms bear an uncanny resemblance. These similarities mean Diamondback can reap more savings than rivals in the fast-consolidating oil industry, justifying the combination.

Autry Stephens started the company that would become Endeavor about 45 years ago. He now joins the club of old-guard oil tycoons, like Pioneer Natural Resources’ Scott Sheffield and Hess’s John Hess, in selling out. In doing so, he is fetching a handsome price.

Advertisement

Endeavor produced an estimated 353,000 barrels of oil equivalent per day in 2023’s last three months. That’s about three-quarters as much as Diamondback, which had a market value of some $33 billion including debt prior to the news. Given the companies’ many similarities, value each barrel of Endeavor’s capacity at the same multiple as Diamondback, and the seller would be worth less than $25 billion. Or consider that the buyer is paying $4.7 million per core location, according to TD Cowen, while the market values Diamondback’s locations at $4.1 million. Endeavor has wrested a decent premium from its suitor.

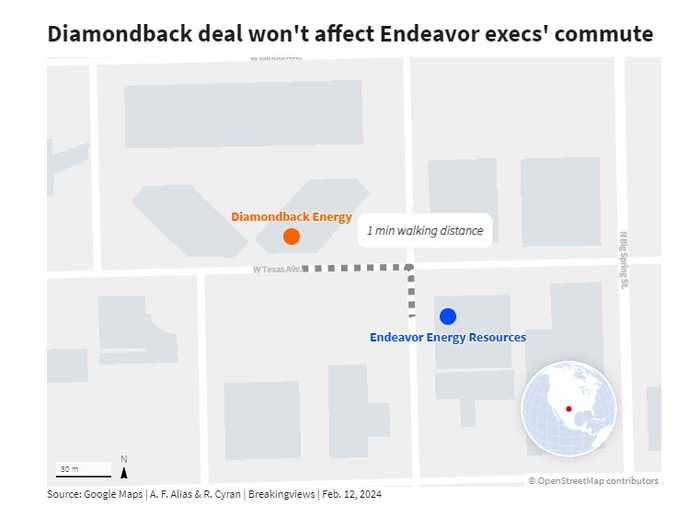

Diamondback can afford it, though. The company says a tie-up should unlock $550 million of annual savings, with a present value of $3 billion over the next decade. That seems plausible. Both firms operate only in the Permian and their acreage is intertwined - some $150 million of the synergies come from combining land. Guidance for the two firms’ combined capital spending in 2025 comes in at $700 million less than their current separate plans for this year, yet production will be roughly the same. Achieving these savings doesn’t even require a longer commute: the companies’ Texas headquarters are a block apart.

Advertisement

The cash-and-shares deal leaves Diamondback investors with over 60% of the combined firm – and therefore nearly $2 billion of the value of the synergies. That more than covers the implicit premium being paid.

Advertisement

Investors look happy, sending the buyer’s shares up nearly 10% Monday morning and adding almost $3 billion to its valuation. Competition to partake in the oil consolidation wave - like Exxon Mobil’s $65 billion Pioneer Natural Resources deal, or Chevron’s $60 billion Hess purchase - could have incentivized reckless dealmaking, especially since Endeavor is one of the biggest remaining independents located in the heart of America’s shale boom. Diamondback and Endeavor's neighborly resemblance defrays that risk, but captures the reward.

13:44 IST, February 13th 2024