Published 16:03 IST, December 21st 2023

Green investors will learn the art of stockpicking

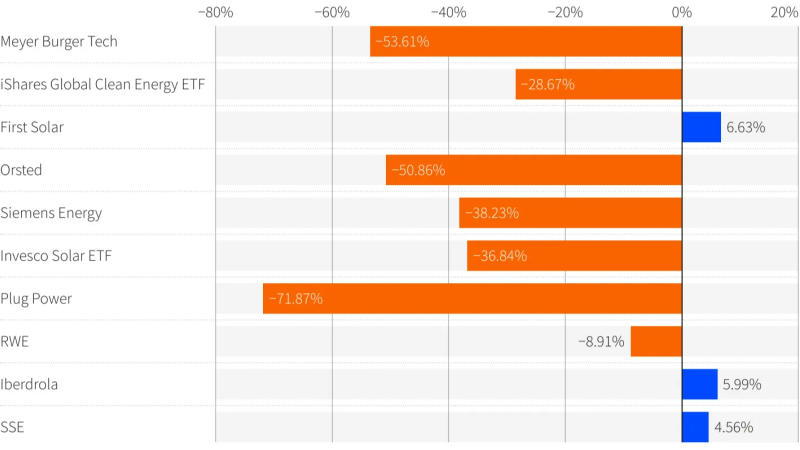

Green stocks have had a close inverse link to bond yields of late

Renewable stocks' performance | Image:

Reuters Breakingviews

- Listen to this article

- 3 min read

Advertisement

16:03 IST, December 21st 2023